Life insurance is a very popular financial product in France. It enables you to protect your family in the event of death, while benefiting from savings. However, this formula is not without disadvantages. It's important to understand the advantages and disadvantages of life insurance before taking out a policy. In this article, we will review the positive and negative aspects of this type of investment.

Life insurance: advantages and disadvantages.

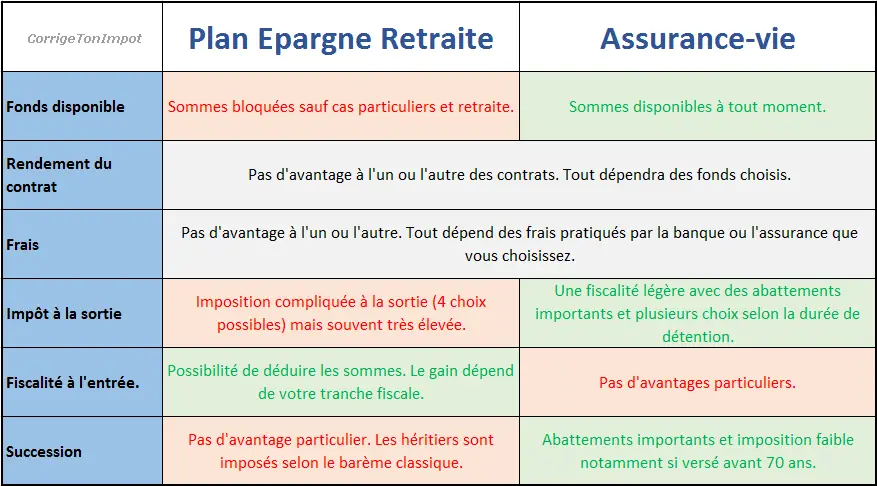

Life insurance is an investment product offering a number of advantages. First and foremost, it offers tax advantages when capital is transferred. Sums paid out to the beneficiary after the policyholder's death are exempt from inheritance tax, up to a certain ceiling.

It also offers great flexibility of use, since the saver can choose to recover all or part of his capital at any time. What's more, life insurance can be used to finance projects such as the purchase of a home or the creation of a business.

However, it should be noted that there are a number of disadvantages associated with this investment product. Firstly, the fees associated with underwriting and managing the contract can be high, which can reduce the final return.

What's more, the capital invested is not guaranteed and may therefore suffer losses as a result of fluctuations in the financial markets. Finally, the contract's exit procedures can be complex, entailing additional charges and taxes.

In short, life insurance offers tax advantages and flexibility of use, but also risks and charges that can impact final returns.

The life insurance trap is closing.

[arve url="https://www.youtube.com/embed/OlqS8gorht8″/]

LIFE INSURANCE EXPLANATION: How does life insurance work in 2023?

[arve url="https://www.youtube.com/embed/Tju6C34sGHM "/]

What are the disadvantages of life insurance?

The major drawback of life insurance is its lack of immediate liquidity. In fact, sums invested in life insurance are blocked for a certain period of time and cannot be withdrawn without penalty. What's more, the cash surrender value of a life insurance policy may be lower than the sum invested, due to the high charges levied by the insurer.

Another disadvantage is the risk of losing the funds invested. Although life insurance is often presented as a safe financial product, there is always a risk that the funds invested may not yield as much as expected, or may even suffer a loss. It is therefore important for investors to understand the risks associated with life insurance before investing their money.

Finally, the tax advantages of life insurance may also be limited in certain cases. For example, if the sums invested in life insurance exceed a certain ceiling, the returns generated will be subject to income tax. It is therefore important for investors to take these tax limits into account when deciding to invest in life insurance.

Is life insurance worth having?

Life insurance is an attractive option for several reasons. Firstly, it allows you to plan for the future and protect your family in the event of your death. By taking out life insurance, you can designate a beneficiary who will receive a lump sum in the event of your death. This can help your family cope financially with unexpected expenses.

What's more, life insurance also offers tax advantages. Capital paid out in the event of death is not subject to income tax, and may also be exempt from inheritance tax up to a certain amount. In addition, sums invested in a life insurance policy can benefit from an advantageous tax framework, depending on the length of time the policy is held.

However, it's important to choose life insurance carefully, based on your objectives and needs. It is also advisable to find out about the different types of contracts offered by insurance companies, as well as their management and remuneration terms and conditions. In short, life insurance can be an interesting solution for protecting your family and optimizing your tax situation, but it's essential to get informed and choose your policy wisely.

Why am I experiencing losses on my life insurance?

Life insurance losses can be caused by a number of factors:

1. The financial market in general: If investments made through life insurance are affected by market fluctuations, then you may suffer losses. This is particularly true if a significant proportion of your investments are in equities or bonds.

2. Investment quality: If life insurance investments have not been carefully selected, or if they have not performed as well as expected, this can lead to losses.

3. Life insurance costs: The various options and benefits offered by life insurance can also involve additional costs that can have a negative impact on your life insurance contract.

So it's important to keep a close eye on the performance of your investments and understand all the costs associated with your life insurance policy to minimize potential losses.

What are the advantages of keeping life insurance?

There are many advantages to keeping life insurance:

- Firstly, it allows you to build up long-term savings to finance a future project, such as buying a property or financing your children's education.

- Secondly, life insurance enables you to pass on capital to your loved ones in the event of your death, while benefiting from tax advantages.

- It also offers great flexibility in managing your savings, with the possibility of modifying the amount of payments and beneficiaries at any time.

- Finally, life insurance can be used to diversify your assets, by investing in different financial vehicles according to your objectives and investor profile.

To sum up, keeping life insurance offers a number of financial, tax and estate planning advantages.

What are the advantages and disadvantages of taking out life insurance?

Life insurance is a savings product with a number of advantages and disadvantages for policyholders.

The benefits:

- Financial security: life insurance allows you to build up savings over the long term, protecting your beneficiaries in the event of your death.

- Flexibility: funds can be withdrawn at any time, without fees or penalties.

- Tax advantages: some life insurance products offer tax advantages, particularly in terms of capital gains tax exemption.

- Easier inheritance: life insurance allows you to pass on your assets to your heirs, avoiding the costs and formalities associated with inheritance.

Disadvantages:

- High charges: life insurance contracts can carry high charges, particularly in terms of entry and management fees.

- Time-consuming to set up: taking out a life insurance policy requires you to complete a number of administrative formalities, which can prove tedious.

- Variable performance: the profitability of life insurance products is variable, depending on fluctuations in the financial markets.

- Tax benefits may change: the tax benefits associated with life insurance products may be modified by current tax laws.

In conclusion, taking out life insurance can be an attractive way of building up long-term savings and facilitating the transfer of your estate.But this has to be seen in the context of the advantages and disadvantages of this savings product.

How to choose life insurance based on its advantages and disadvantages?

Life insurance is a highly popular financial instrument, offering tax-advantaged ways of capitalizing and passing on money. However, it is important to understand the advantages and disadvantages of this solution so as to choose the one that best suits your profile.

The advantages of life insurance :

- The possibility of designating a beneficiary to receive the capital in the event of death: this allows you to pass on a capital sum to your loved ones without them having to pay inheritance tax, within the limits of the legal framework in force.

- Tax benefits: life insurance offers tax advantages on inheritance and policy surrender. Interest earned is also tax-exempt under certain conditions.

- Great flexibility: life insurance is a flexible, modular product that can be adapted to the investor's needs in terms of management, payments and choice of options.

The disadvantages of life insurance :

- High fees: life insurance contracts can carry high management and entry fees, which eat into the contract's performance.

- Variable profitability: returns on life insurance policies can be unpredictable, depending in particular on the quality of the insurer's investments. There is no guaranteed return.

- Risk of capital loss: unlike a savings account, life insurance is not risk-free. The sums invested can be lost if the insurer goes bankrupt.

When choosing a life insurance policy, you need to take all these factors into account, as well as your objectives and needs in terms of savings and inheritance. It's important to get information from several insurers and compare offers before making your choice.

What are the tax advantages and disadvantages of life insurance in France?

Tax benefits :

- Gains earned on a life insurance policy are not taxable as long as they remain in the policy. This means that money invested in life insurance can grow without being subject to income tax.

- In the event of the policyholder's death, the beneficiaries of the life insurance policy benefit from an allowance of 152,500 euros on the sums paid in.

- Life insurance premiums can be deducted from income tax under certain conditions.

Disadvantages :

- If the policyholder surrenders all or part of the contract, the tax burden can become very heavy. In this case, the interest received will be subject to income tax or the single-rate withholding tax (prélèvement forfaitaire unique or PFU).

- The costs of taking out a life insurance policy can be high.

- Life insurance is a long-term investment, not suitable for all investor profiles.

It is therefore advisable to think carefully before taking out life insurance, and to consult a wealth management advisor.

In conclusion, life insurance offers advantages and disadvantages that should be taken into account before taking out a policy. On the one hand, it enables you to protect your family and prepare your estate, while benefiting from attractive tax advantages. On the other hand, it can involve high costs and limited profitability in some cases. So it's important to compare offers carefully, and to think about your objectives before taking the plunge. In short, life insurance remains a useful tool for planning your financial future, but you need to understand its mechanisms and implications to get the most out of it.