Long-term debt comprises benefits and disadvantages. Discover the implications of taking on debt over an extended period in our article examining the various facets of this financial decision.

Surviving credit

[arve url="https://www.youtube.com/embed/v8eM5nQviL4″/]

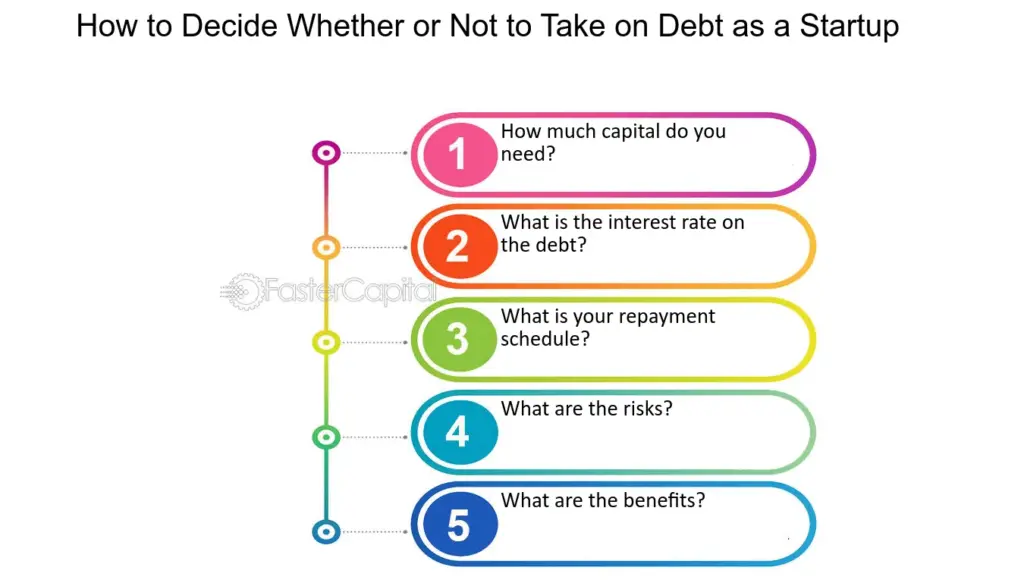

What are the advantages and disadvantages of debt?

Debt can have advantages and disadvantages in today's context. Here are a few to consider:

Benefits of debt :

1. Project financing : Debt can enable companies and governments to finance major projects such as infrastructure construction, technology development or social programs.

2. Economic growth : Debt can stimulate economic growth by injecting liquidity into the economy. This can support investment, create jobs and stimulate consumption.

3. Financial flexibility : Debt can offer financial flexibility by enabling borrowers to manage their cash flows and allocate resources to different needs, depending on market conditions.

Disadvantages of debt :

1. Repayment and interest : The main disadvantage of debt is that it has to be repaid with interest. This can increase the borrower's financial burden and reduce his or her ability to invest in other areas.

2. Dependence on creditors : When a country or company goes into debt, it becomes dependent on its creditors to finance its activities. This can limit its sovereignty and freedom of decision in certain cases.

3. Risk of overindebtedness : Too much debt can lead to long-term solvency problems. If borrowers fail to repay their debts, this can lead to financial crises and cuts in public spending.

It's important to note that the advantages and disadvantages of debt can vary according to the specific economic, political and social context. It is therefore essential to analyze each situation carefully.

What are the consequences of debt?

Debt has many harmful consequences, both for individuals and for the economy as a whole. On a personal noteExcessive indebtedness leads to financial difficulties, reduced purchasing power and a deterioration in quality of life. People in debt often face repayment problems, which can lead to foreclosure, eviction or financial penalties.

At the economic levelExcessive indebtedness can lead to financial instability. When households, businesses and even governments are heavily indebted, this can lead to widespread financial fragility. This can lead to reduced investment, lower consumption and economic stagnation.

What's more, indebtedness can lead to growing social inequalities. People with limited access to credit find it more difficult to invest in education, health or entrepreneurship, reinforcing economic and social disparities.

FinallyIt's important to remember that debt can have long-term consequences. Accumulated debts can add up and become increasingly difficult to repay, leading to a perpetual cycle of indebtedness for individuals and governments alike.

In conclusion, excessive indebtedness has harmful consequences at both individual and economic levels, and it is essential to promote responsible financial management to avoid these problems.

Why do you need to be in debt?

It's important to note that my answer is based on a hypothesis, as your question is very general and doesn't specify the specific context regarding debt. However, I will try to give you some possible reasons why some people may consider it necessary to be in debt.

1. Investment: One of the most common reasons why some people choose to take on debt is investment. For example, borrowing money to buy a house or property can be seen as a long-term investment, as the value of these assets tends to increase over time. Similarly, some entrepreneurs may take out loans to finance their business projects, in the hope of future profits.

2. Education: Debt can also be seen as a necessary choice to finance education. Higher education can be expensive, and many students have to take out student loans to cover the cost of tuition, books, accommodation, and so on. In this case, debt is seen as an investment in knowledge and skills that could translate into better job prospects and income in the future.

3. Financial emergencies: Sometimes, people may be forced into debt due to unforeseen circumstances, such as medical emergencies or urgent home or car repairs. In such cases, debt can be seen as a way of coping with difficult financial situations and stabilizing one's situation.

It's important to stress that not all types of debt are beneficial and can have negative consequences. Before taking out a loan, it's essential to carefully assess your ability to repay, and to understand the conditions and interest involved.

How can you use debt to get rich?

Using debt to build wealth is risky and not recommended. Debt can be a useful financial tool when used responsibly, but it's important to understand the consequences and risks associated with this strategy.

The first thing to consider is the interest rate on the debt. If you borrow money at a high interest rate, it may be difficult to generate enough return to cover these costs. It's best to look for low interest rates or negotiate favorable terms before borrowing.

The second essential element is the choice of investment project. When using debt to invest, it's advisable to choose projects that have a strong chance of success and a high potential return. This could be a real estate investment, a business start-up or any other project with promising prospects.

Debt management is also crucial. It's important to make regular repayments to avoid falling into a spiral of debt. It's advisable to monitor your finances regularly and maintain rigorous financial discipline.

Finally, it is essential to diversify your investments. The golden rule of investing is not to put all your eggs in one basket. By diversifying your investments, you minimize the risks associated with a single opportunity.

It's important to remember that using debt to build wealth carries significant risks and can lead to serious financial consequences if mismanaged. So it's essential to exercise caution, do thorough research before borrowing, and consult a professional financial advisor if necessary.

In conclusion, using debt to build wealth is a risky business. It's best to rely on sound, responsible investment strategies to build long-term wealth.

In conclusion, taking on long-term debt has both advantages and disadvantages. On the one hand, it enables you to finance major projects such as buying a house or a car, by spreading repayments over a longer period. It can also offer a degree of financial stability, as monthly repayments are generally lower.

HoweverHowever, it's important to note that taking on long-term debt also entails risks. Cumulative interest payments can be considerable, adding to the financial burden. What's more, it limits future borrowing capacity, which can be problematic if other financial needs arise.

That's why it's crucial to think carefully before taking on any long-term debt, by carefully assessing your ability to repay and considering possible alternatives. We recommend that you consult a financial professional for an objective analysis of your situation, so that you can make an informed decision.

All in allLong-term debt can be a practical solution for certain projects, but you need to be aware of the potential risks and manage your finances responsibly.